In recent months, leading technology companies have dominated the stock market, largely due to their forays into the artificial intelligence (AI) sector.

Looking ahead to the second half of 2024, investors are closely watching semiconductor giants Nvidia (NASDAQ: NVDA) and Qualcomm (NASDAQ: QCOM) to see which stock offers the more promising opportunities.

Both Nvidia and Qualcomm are well positioned in the technology landscape, but their different market focuses and valuation metrics suggest different prospects for the coming months.

Nvidia’s dependence on TSMC’s (NYSE: TSM) facilities in Taiwan adds further uncertainty, especially amid rising geopolitical tensions following Donald Trump’s comments on Taiwan and U.S. defense commitments.

Meanwhile, Qualcomm continues to struggle with a weakened smartphone market, which has impacted the company’s growth over the past three years.

Given the current market conditions, investors are considering whether Nvidia or Qualcomm offers better opportunities for the second half of 2024. To answer this question, Finbold asked ChatGPT-4o for insights into which stock is expected to deliver the best performance.

Nvidia shares

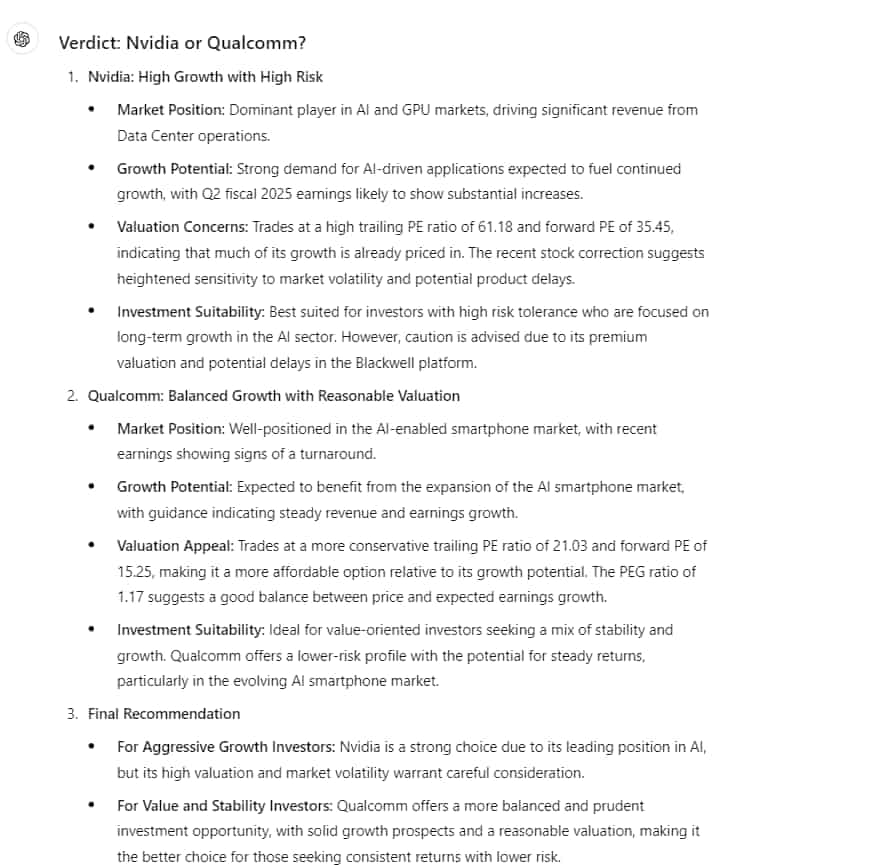

Nvidia has excelled in the technology sector, particularly due to its dominance in the AI and GPU markets.

However, Nvidia stock has been under significant pressure recently, losing nearly 26% from its 52-week high and losing about 20% in just one month. This decline can be attributed to macroeconomic uncertainty, a broader sell-off in technology stocks and concerns about the company’s high valuation.

To make matters worse, reports suggest there could be possible delays in the launch of Nvidia’s next-generation Blackwell platform due to design flaws.

While these delays could impact future performance, Nvidia’s results for the second quarter (Q2) of fiscal 2025, scheduled for release on August 28, 2024, are expected to show strong growth due to AI-driven demand.

Nvidia’s data center revenues have been a key driver of its financial performance. In the first quarter (Q1) of fiscal 2025, Nvidia reported data center revenues of $22.6 billion, a 427% year-over-year increase.

The company has forecast total revenue of around $28 billion for the second quarter, a 107% improvement year over year. Analysts expect Nvidia’s earnings per share (EPS) to more than double in the second quarter, reflecting strong demand for AI-driven applications.

However, Nvidia’s high valuation remains a cause for concern. The stock trades at a P/E ratio of 61.18 and a P/B ratio of 35.45. Despite the recent correction, Nvidia’s market capitalization is still a staggering $2.57 trillion.

The PEG ratio of 1.19 suggests that the stock is expensive relative to its growth potential, so investors should be cautious about entering at current levels, especially given the looming delays to the Blackwell platform.

Qualcomm shares

Qualcomm, which has traditionally focused on the smartphone chip market, is repositioning itself as a major player in the emerging AI-enabled smartphone segment.

The company’s latest results for the third quarter of fiscal 2024 indicate a turnaround, with revenue up 11% year-over-year to $9.4 billion and adjusted earnings per share up 25% to $2.33 per share. Qualcomm’s optimistic forecast for the current quarter, with expected revenue growth of 14% year-over-year, further strengthens the outlook.

Qualcomm is likely to benefit from the expansion of the AI smartphone market, which is expected to grow significantly in the coming years. This strategic positioning could lead to significant revenue and profit growth, making Qualcomm an attractive investment for those seeking both stability and growth.

From a valuation perspective, Qualcomm’s valuation is more conservative than Nvidia’s. The stock trades at a trailing P/E of 21.03 and a leading P/E of 15.25, making it significantly cheaper than Nvidia.

With a market cap of $183.23 billion and an enterprise value of $184.75 billion, Qualcomm has a strong financial position with minimal debt concerns. The PEG ratio of 1.17 suggests the stock is fairly valued relative to its growth potential.

ChatGPT’s verdict on the best stock

Finally, ChatGPT-4o emphasized that both Nvidia and Qualcomm offer solid investment opportunities with strong growth potential, especially in the AI sector.

Nvidia offers significant growth potential in the booming AI market, but due to its high valuation and recent price correction, it also comes with high risks and is therefore only suitable for investors with a high risk appetite.

On the other hand, Qualcomm’s balanced growth and reasonable valuation make it a better fit for value investors looking for stability with growth potential in the AI-enabled smartphone market.

Nvidia is ideal for aggressive growth seekers, while Qualcomm is a more suitable choice for those who prefer a balanced approach.

Investors should weigh their risk appetite and investment objectives when deciding between these two technology giants.

Disclaimer: The content of this website does not constitute investment advice. Investments are speculative. When you invest, your capital is at risk.