")

Thomas Barwick/DigitalVision via Getty Images

Investment thesis

Louisiana Pacific Corporation (NYSE: LPX) should continue to deliver good growth in the future. Despite macroeconomic challenges, the company is focused on further increasing its share by investing in capacity expansion, sales force and marketing. The company’s partnership with Lennar (LEN) is driving growth of its BuilderSeries product line and may employ a similar strategy with other construction companies to win business, which bodes well for the company’s revenue growth. The company’s revenue should also benefit from a potential recovery in the housing market once the interest rate cycle reverses in the coming months. The outlook for the R&R market is also attractive as the existing residential property inventory is aging, which should support revenue growth in the medium to long term.

On the margin side, the company’s margins should benefit from volume leverage, especially if the interest rate cycle changes in the coming months. In addition, lower Raw material costs and the company’s shift to higher-margin siding and value-added OSB businesses should also support margin growth. In addition, the company’s investments in automating its manufacturing facilities to increase efficiency should help margin expansion in the long term. In terms of valuation, the stock trades at a discount to rival James Hardie Industries plc (JHX). If the company continues its good performance, I believe its valuation multiple can be set higher to be in line with JHX. Given the company’s strong growth prospects and the potential for a re-rating of the valuation multiple, I recommend the stock as a buy.

Sales analysis and outlook

In my previous article in May 2024, I highlighted the company’s strong growth prospects, benefiting from its solid execution and market share gain prospects in the cladding and value-added OSB sectors, as well as attractive long-term fundamentals in the residential market. The company has since reported its second quarter 2024 results and similar dynamics were seen there.

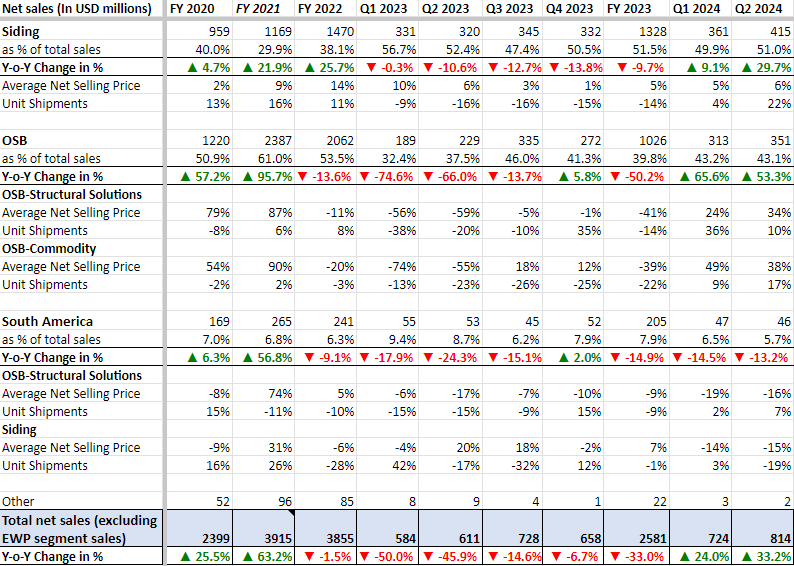

In the second quarter of 2024, the Company’s revenue increased 33.2% year-over-year to $814 million, supported by volume and price increases in both the Siding and OSB segments, which effectively offset the revenue decline in the LP South America (LPSA) segment.

In the facade cladding segment, sales increased by 29.7% year-on-year, driven by price increases and higher volumes. The completion of last year’s capacity expansion projects and inventory reductions in distribution channels, as well as increased market share gains in the repair and remodeling market, led to volume growth of 22% year-on-year. Unit prices also increased by 6% year-on-year due to list price increases and a favorable mix.

In the OSB segment, sales increased by 53.3% year-on-year, driven by a 34% year-on-year price increase and an improved mix of structural solutions.

On the other hand, the LP South America (LPSA) segment recorded a 13.2% year-on-year decrease in revenue due to a 16% decrease in the average selling price (ASP) of OSB Structural Solutions and a 15% decrease in the ASP of the Siding business. Unfavorable currency fluctuations and a 19% volume decrease in the Siding business also negatively impacted revenue growth. These negative factors were partially offset by a 7% volume increase in the OSB Structural Solutions business.

LPX historical net sales growth by segment (Company data, GS Analytics Research)

Louisiana-Pacific was able to achieve strong revenue growth last quarter despite a high interest rate environment and subdued demand in the repair and remodeling markets. The company’s strategic initiatives to gain market share in the siding business are working well. In my last article, I shared my expectations for good growth for the company, driven by its recent partnership with Lennar (LEN) and Home Depot (HD). This has worked out well for the company, and at the last earnings call, management noted market share gains in both the new construction and R&R markets.

I expect the company to outperform its end markets in the future by continuing to gain market share. The company continues to invest in expanding its sales team in both new construction and repair and remodeling to communicate the benefits of its value-added offering to prospective customers. The company has also invested in converting its existing OSB capacity to siding plants as well as opening new siding capacity. This should help it meet the increasing demand for its products while it continues to gain market share.

An interesting aspect of the company’s partnership with Lennar was that it was able to leverage its position as a leading supplier of OSB products to Lennar to win contracts for BuilderSeries products. The company has entered into supply contracts for its OSB products with several other major construction companies and can use a similar strategy with other construction companies to win business.

Management remains confident that share prices will continue to rise. At the company’s last earnings call, CEO Brad Southern said:

We believe we have significant growth potential and market share gains in the new construction, R&R and offsite siding business, as well as in Prime and pre-engineered SmartSide products. And we intend to continue to develop new products, expand our target markets and execute our sales and operations strategies to drive future growth.

The longer-term fundamentals for new construction as well as the R&R market also remain solid, which bodes well for the company’s growth. The significant shortage of new construction following the great housing recession of 2008 has created a tight demand-supply situation in the market. As such, I expect the new construction sector to recover quickly once the interest rate cycle reverses in the coming months. The demand drivers for repairs and remodels remain intact even with aging existing housing stock, which should support medium to long-term growth.

Overall, I remain optimistic about the company’s short-term and long-term prospects.

Margin analysis and outlook

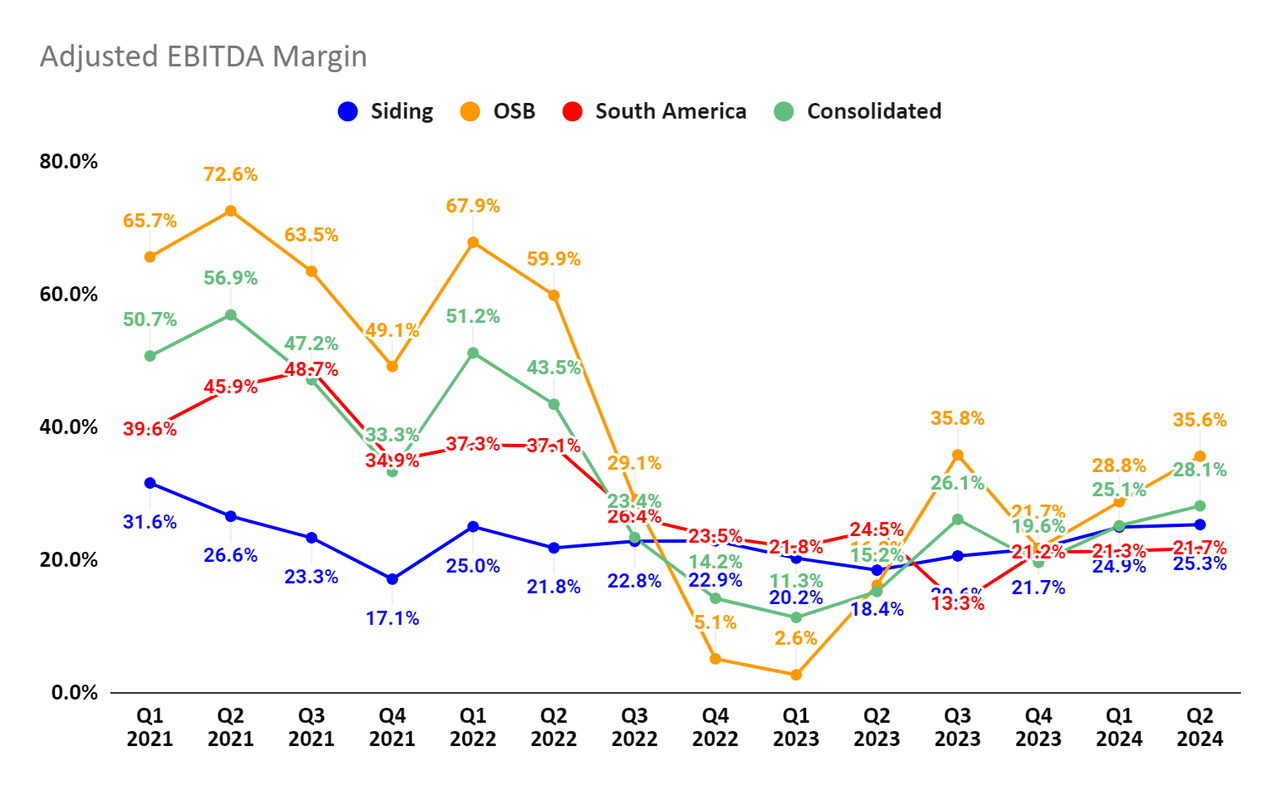

In the second quarter of 2024, LPX’s adjusted EBITDA margin increased 1,290 basis points year-over-year to 28.1% due to price and volume increases.

In the Siding segment, adjusted EBITDA margin increased 690 basis points year-over-year to 25.3%, reflecting higher sales and lower freight, raw material and labor costs, partially offset by higher overhead costs.

The OSB segment’s adjusted EBITDA margin increased 1,950 basis points year-over-year to 35.6%, reflecting the impact of higher prices and volumes, partially offset by higher factory costs. The company is making targeted investments in new technologies to modernize its production facilities, resulting in a 30% increase in operating efficiency.

LPSA’s adjusted EBITDA margin decreased 280 basis points year-on-year to 21.7% due to unfavorable currency movements.

LPX adjusted EBITDA margins (Company data, GS Analytics Research)

The company’s margin outlook is positive. The company’s margins should benefit from volume leverage, especially as interest rate cycles reverse in the coming months. Commodity prices, including lumber and resin prices, are also trending downward and should have a positive impact on margins. In addition, as the company transitions from commodity OSB to higher-quality OSB and siding, margins should become less volatile and experience structural improvements.

Margins on Expert Finish products are currently below the company average due to the company’s development and inefficiencies, but should improve and converge to the company average in the long term. The company is also investing in the automation of its production facilities, which should lead to efficiency gains and improve margins in the long term.

Evaluation and rating

LPX stock trades at EV/EBITDA (TTM) of 9.65x and EV/EBITDA (FWD) of 11.24x, a discount to peer James Hardie Industries plc (JHX), which makes fiber cement-based siding and other building products and trades at EV/EBITDA (TTM) of 14.16x and EV/EBITDA (FWD) of 14.77x.

LPX’s wood siding is less expensive, easier and faster to install, and offers similar durability. These advantages, along with good execution that is helping LPX gain market share, should help the company’s valuation multiple rise to JHX’s level. Given the company’s strong growth prospects and the potential for a valuation multiple re-rating, I recommend buying LPX stock.

Risks

- Although the Company is reducing its dependence on the standard OSB business, it still represents a significant part of the current portfolio and fluctuations in OSB prices could impact the Company’s profitability.

- The Company’s revenues are primarily based on the North American new construction, repair and remodel markets. These markets are cyclical and are affected by changes in macroeconomic conditions and interest rates. Any adverse developments on these fronts may impact the Company’s revenue growth.

Take away

LPX has good prospects for revenue and margin growth. I expect the company to continue to gain market share and outperform in the end market given its good execution and investments in capacity expansion, sales team, and marketing. In addition, the company’s revenue growth should benefit from its partnership with Lennar (LEN), which should help it gain market share. In addition, the recovery in the housing market as the interest rate cycle reverses in the coming months should also contribute to revenue growth. The long-term fundamentals of the R&R market remain intact even with an aging existing home inventory. Margins should also expand with the help of volume levers, a mix shift toward high-margin siding and value-added OSB businesses, and the investments to increase efficiency. This, coupled with the potential for a re-rating of the valuation multiple as the company continues its good execution, makes LPX stock a good buy.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.