strong earnings are a good indicator of the company’s strength")

When companies post strong earnings, stocks generally perform well, just like The (WSE:LEG) stock has improved recently. We have done some analysis and found several positive factors besides the earnings numbers.

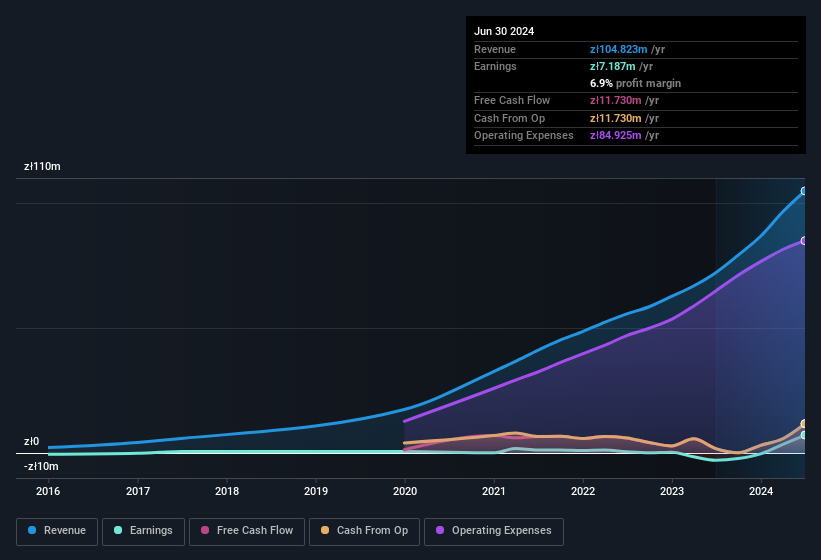

Check out our latest analysis for Legimi

A closer look at Legimi’s earnings

Many investors have never heard of the Accrual ratio from cash flowbut it is actually a useful measure of how well a company’s profit is covered by free cash flow (FCF) during a given period. The accrual ratio subtracts FCF from profit for a given period and divides the result by the company’s average funds from operations during that period. This ratio indicates how much of a company’s profit is not covered by free cash flow.

Therefore, it is actually considered good if a company has a negative accrual ratio, but bad if its accrual ratio is positive. While it is not a problem to have a positive accrual ratio, indicating some level of non-cash profits, a high accrual ratio is arguably a bad thing because it indicates that there is no cash flow to match accounting profits. To quote a 2014 paper by Lewellen and Resutek, “Companies with higher accruals tend to be less profitable in the future.”

Legimi has an accrual ratio of -8.28 for the year to June 2024. As a result, its statutory profits were much lower than its free cash flow. That is, it generated free cash flow of PLN 12 million during the period, dwarfing its reported profit of PLN 7.19 million. Legimi shareholders are no doubt pleased to see that free cash flow has improved over the past twelve months. In particular, the company has issued new shares, diluting existing shareholders’ interest and reducing their share of future profits.

Note: We always recommend investors to check balance sheet strength. Click here to access our balance sheet analysis of Legimi.

A key aspect of assessing the quality of earnings is to look at how much a company dilutes shareholders. Legimi increased the number of shares outstanding by 31% last year, so each share now receives a smaller share of the profit. Talking about net income without considering earnings per share is to get distracted by the big numbers and ignore the smaller numbers that are important for per share Value. View Legimi’s historical EPS growth by clicking this link.

What impact does dilution have on Legimi’s earnings per share (EPS)?

We don’t know how much the company made or lost three years ago because we don’t have the data. And even if we focus only on the last twelve months, we don’t have a meaningful growth rate because it was also losing money a year ago. But math aside, it’s always good to see a formerly unprofitable company get back on track (though we admit that earnings would have been higher had dilution not been necessary). So you can see that dilution has had a pretty significant impact on shareholders.

If Legimis returns long-term per share can rise, then the share price should rise. On the other hand, we would be far less enthusiastic if we were told that earnings (but not earnings per share) were improving. For this reason, one could say that earnings per share are more important than net income in the long run, assuming the goal is to assess whether a company’s share price might rise.

Our assessment of Legimi’s earnings development

To summarize, Legimi has strong cash flow relative to earnings, suggesting high-quality earnings, but dilution means earnings per share are declining faster than profits. Based on these factors, we believe Legimi’s earnings are a fairly conservative indicator of its underlying profitability. If you want to dive deeper into Legimi, you should also examine what risks the company is currently facing. In terms of investment risks: We have identified 3 warning signs with Legimi, and understanding these should be part of your investment process.

Our research into Legimi has focused on certain factors that can make the company’s earnings look better than they are. However, there are many other ways to form an opinion about a company. For example, many people consider a high return on equity to indicate a favorable business situation, while others like to “follow the money” and look for stocks that insiders are buying. Although this may require a little research, you may find free Collection of companies with high return on equity or this list of stocks with significant insider holdings may prove useful.

New: AI Stock Screeners and Alerts

Our new AI Stock Screener scans the market daily to uncover opportunities.

• Dividend powerhouses (3%+ yield)

• Undervalued small caps with insider purchases

• Fast-growing technology and AI companies

Or create your own from over 50 metrics.

Try it now for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.