")

Jonathan Knowles

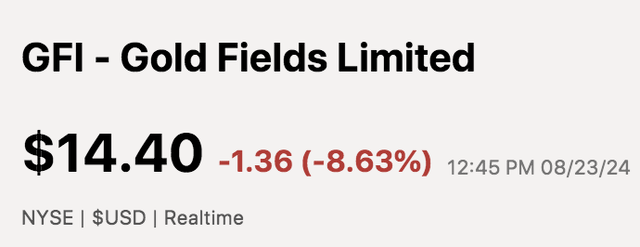

Goldfields Limited (NYSE: GFI) released its half-year results on Friday, announcing disappointing numbers and a downgrade of its annual forecast. Investors did not like the news, with Gold Fields shares falling almost 10% following the event.

GFI share price (Search Alpha)

We last covered Gold Fields stock in June, reiterating our neutral view on its prospects. However, given Gold Fields’ turbulent quarter and the market’s subsequent reaction, I have decided to update our thesis and comment on the first half results.

This is my opinion on Gold Fields stock.

A memory of gold fields

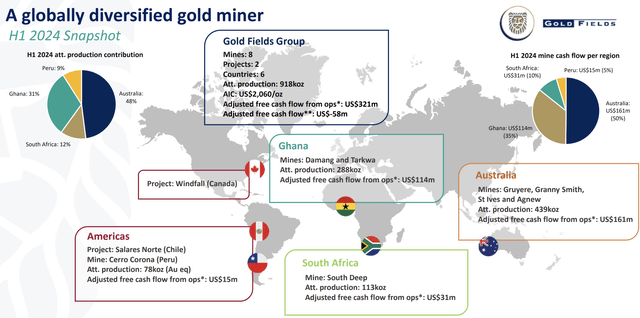

For those who don’t know, Gold Fields is a South African gold mining company with operations in South Africa, West Africa, Australia, Canada and Peru.

The following chart provides Gold Fields’ cash flow and production mix.

Operational framework (Goldfields)

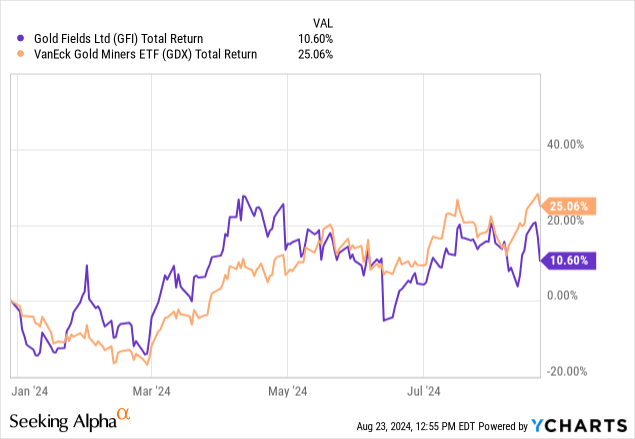

Although since the At the turn of the year, Gold Fields underperformed the VanEck Gold Minders ETF (GDX), suggesting that there are notable idiosyncratic variables.

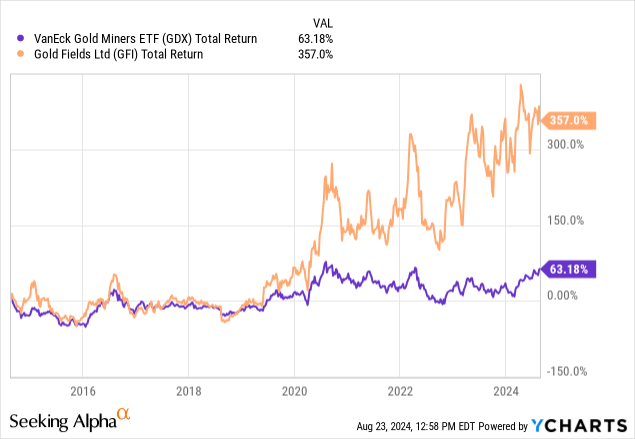

I’ve included a longer-term return below to provide a time series perspective. As the chart shows, Gold Fields has outperformed its peer group over the past decade.

Results report

headline

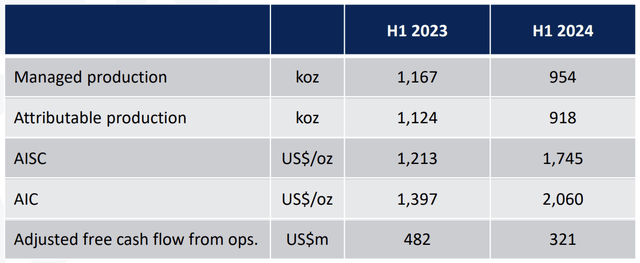

Gold Fields’ managed production for the first half of the year fell approximately 22.3% year-on-year to 954,000 ounces. Likewise, the Company’s attributable production fell approximately 22.4% to 918,000 ounces, while all-in costs increased 43.86% to $1,745 per ounce.

The Company’s combined operating performance ultimately resulted in a decrease in adjusted free cash flow from operations of $161 million compared to the prior year, signaling a downward trend.

Production and financial headlines (Goldfields)

I think it’s safe to say that some may find Gold Fields’ first half results disappointing. However, what were the main causes of Gold Fields’ poor performance? What does the future hold?

Let’s look at some of his turning points and discuss them.

Lower production of Gruyère and St. Ives in Australia

Gruyère production fell 20% year-on-year to 127,000 ounces, primarily due to severe weather that limited mining operations. However, mining resumed in April, meaning production is likely to ramp up again in late 2024.

Aside from that, St IvesProduction fell 25% year-on-year to 139,000 ounces. Gold Fields said the lower production was due to lower grades from underground operations and inventory levels. Despite the headwinds for the mine, Gold Fields expects volumes at St. Ives to recover 49%.

I have little to add about St IvesHowever, I believe the Gruyere collapse was a non-core event and can probably be excluded from Gold Fields’ core earnings.

Lower supply from South Africa’s southern low

Production at the South Deep Mine fell 25% year-on-year to 117,000 ounces, primarily due to a fatal accident in January and “limited access to workings due to increased backfill handling and slow drilling through crushed soil.”

I cannot comment on the technical details, but Gold Fields is expecting volumes to increase by 14%, which I think is credible given that the power outages in South Africa are easing. However, summer is approaching in the region, which may bring rain.

Lower at Peruvian Cerro Corona

Cerro Corona production fell 42% to 79,000 ounces, with the main reason for the decline being weather and related knock-on effects.

Although I think the events are non-core, mining at Cerro Corona will soon cease as the mine approaches its planned maturity date of 2025/2026. Gold Fields will mine reserves after that, but replacing revenue could be an issue as that would likely require an acquisition.

That being said, the production results reported in the main section are what I consider to be material. Gold Fields has other mines – visit this link for a full breakdown.

A few positive aspects

Gold Fields’ operational performance led to a downward revision to its guidance. The company now expects full-year production of 2 to 2.15 million ounces, below its previous guidance of 2.2 to 2.3 million ounces.

Despite the operational headwinds, I see some positive aspects.

Normalization and gold prices

As mentioned in the previous section, there may be a return to normalization of operations, as many of Gold Fields’ failures are due to non-core events such as weather or sub-standard quality.

In addition, gold prices are on the rise and this trend is likely to continue until the end of 2024. Why? A U.S. interest rate turnaround seems likely, and economic indicators such as business confidence, annualized GDP growth and unemployment suggest that systematic risk has increased. Therefore, I expect many traders to use gold to hedge against USD tail risk.

XAUUSD Spot (Search Alpha)

Further links:

- US economic indicators.

- Gold as a hedge for the USD

- USD vs. US interest rates

- Gold to hedge against extreme economic risks

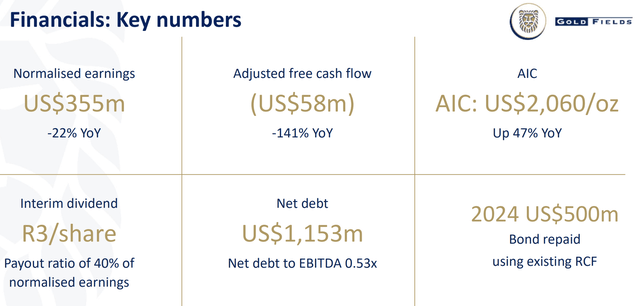

Lucrative dividends

Another feature I find compelling is Gold Fields’ dividend policy, which is 40% of normalized earnings. The stock has an average yield of 2.89% over four years (prior to earnings release). We will likely see a slight decline in Gold Fields’ expected and normalized dividend after the latest release. However, I still consider the dividend to be lucrative and sustainable, especially given the company’s impressive debt coverage.

Apart from that, Gold Fields has a net debt/EBITDA ratio of 0.53, which shows its debt coverage.

Goldfields

Buy on dip?

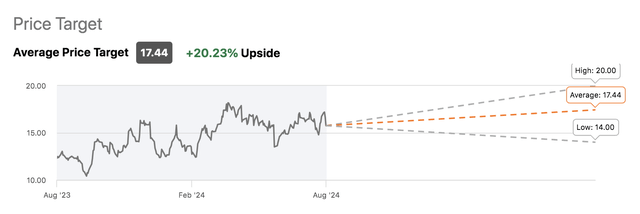

Seeking Alpha tracks Wall Street analysts’ price targets. The tool suggests that the average price target among sell-side analysts is $17.44, representing nearly 20% upside potential.

Price target for GFI shares (Search Alpha)

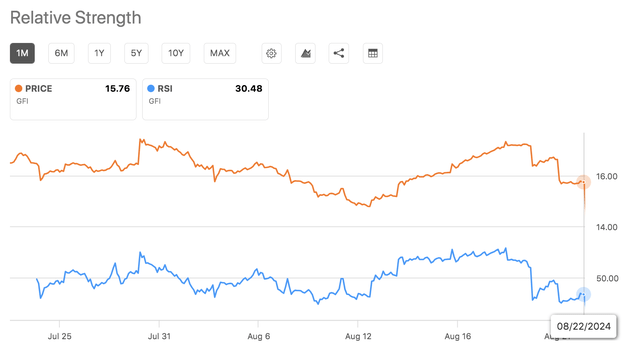

In addition, Gold Fields’ plunge following the earnings release pushed the stock’s Relative Strength Index down to the 30 mark, suggesting that the stock may be oversold (30 is considered the “oversold” limit). Although the RSI is merely a technical indicator, it is used by many to find entry points.

Relative Strength Index (Search Alpha)

Final thoughts

I view Gold Fields stock as an equivalent asset.

Gold Fields’ post-earnings plunge could provide an entry point for some, especially given the potential normalization of the company’s mining activities, Gold Fields’ financial market-based indicators, and the momentum exhibited by the gold price.

However, despite its positive aspects, Gold Field’s catalysts are probably not enough to justify an overweight position.