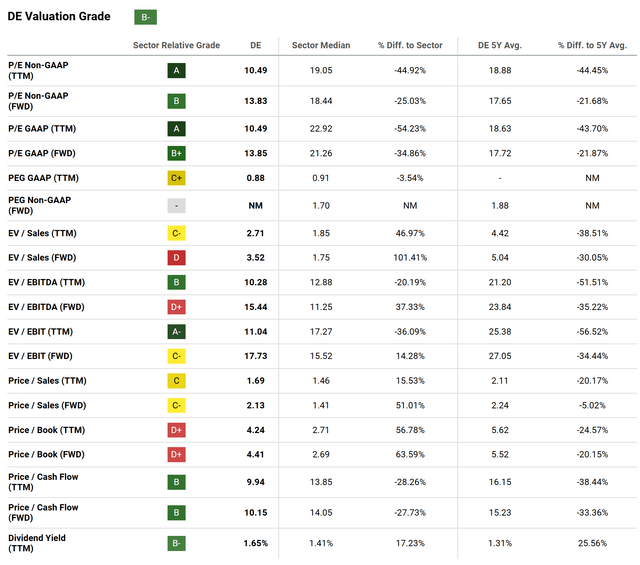

")

Bundit Minramun/iStock Editorial via Getty Images

Following a very strong performance in 2020 and 2021, Deere & Company (NYSE:DE) stocks have had a bumpy ride in recent years.

The company benefited greatly from of the pandemic boom in its core products of tractors, combine harvesters and commercial vehicles, it is clear in retrospect that much of the demand was brought forward due to Covid.

DE’s results in 2022, 2023 and 2024 (so far) were not badThey weren’t earth-shattering either.

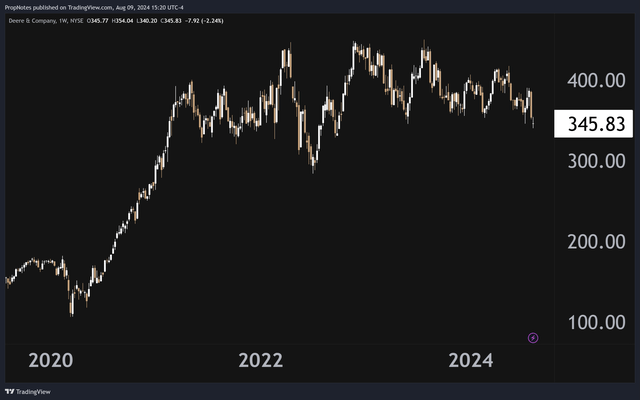

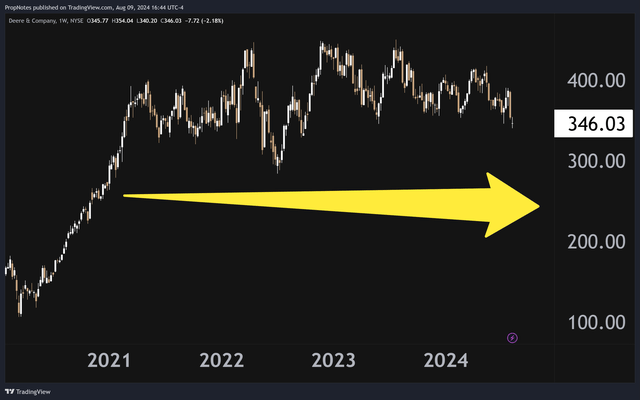

The impact of this pull-forward, as well as a general slowdown in agricultural capital spending, has resulted in slowing revenue growth at DE over the past eight to ten quarters, while the stock has been similarly stagnant during that time:

TradingView

Nevertheless, the company has made business progress during this period. especially at the edgesand the top line shows that have The targets achieved have pushed profitability to a record level.

Should revenue growth recover in the coming quarters – and we expect it to – we see significant upside potential for DE shareholders as the increased margins will have a positive impact on the bottom line. We also see scope for a potential multiple revival.

Todaywe explain why we believe that the company’s incredibly attractive valuation, improved margin profile and potential for renewed revenue growth make DE one of the Top hidden growth stories of the next few years.

Sounds good? Then let’s get started.

Deere’s Finances

As mentioned above, Deere has some interesting years ahead from a financial perspective.

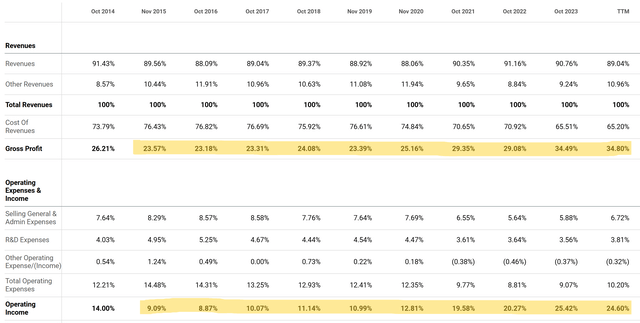

On the one handThe company’s operational execution has been excellent, with the stock’s gross, operating and net margins growing like clockwork over time:

I’m looking for Alpha

This margin and pricing power is largely due to the company’s strong market position, along with a number of economies of scale that DE has been able to exploit as it has grown. Some have called the company’s market position “unfair” and “monopolistic,” but that is something we will leave to the courts to decide. We will also discuss this in more detail in the Risks section.

Management, for its part, is relatively confident about future margin development:

It is worth noting that this quarter’s performance in plant operations Margin of over 21% is one of the best quarters in the company’s historyWe are confident about the start of the year and will focus on implementing our plan in the remaining two quarters.

…

I would like to reiterate this Market cycles are nothing new to usand we have learned from the past, making us a more resilient and better prepared company than ever before. Our proactive management reflects this and shows that we are structurally better today than companies with equipment Margin forecast just over 18% despite unfavorable mix in a rapidly changing global environment. And as a result, we feel that we are moving into the best possible position for the future.

It is clear to us that management has done a good job in terms of cost management, inventory management and accurate market forecasting.

All this saidRevenue growth was lacking as weaker spending on agricultural equipment led to a slight decline in product sales volumes compared to the previous year. Management expects this trend to continue through the end of fiscal 2024.

Some of this is due to Covid and Covid-related distortions, as we have discussed, but some of it is also due to long-term micro factors within the equipment market more broadly. Some of these include:

10 questions

In our view, sales are likely to pick up again in the coming quarters due to the increased aging of the US machinery fleet and the strong balance sheet situation of the US agriculture industry, which should lead to an improvement in the volume of upcoming upgrades.

Adding these factors to the general cyclicality of producer margins, we see improvements in sales growth in DE likely to occur by mid-2025. last.

Not taken into account in previous forecasts is the fact that DE’s recent business shift towards a technology and services layer in addition to current products could also make a significant contribution to revenue in the coming years. Management has forecast a TAM of 150 billion for this market, which seems high to us, but we also expect a positive upturn in the second half of the decade.

Looking at Thursday’s earnings, estimates put earnings per share at $5.88 per share, which seems a little low to us given the tailwinds mentioned above. It is true that agricultural spending has was weak, but we are not as sure as everyone else that it will continue like this.

What is particularly important to observe is the mood and spending in agriculture as well as new progress in the services sector.

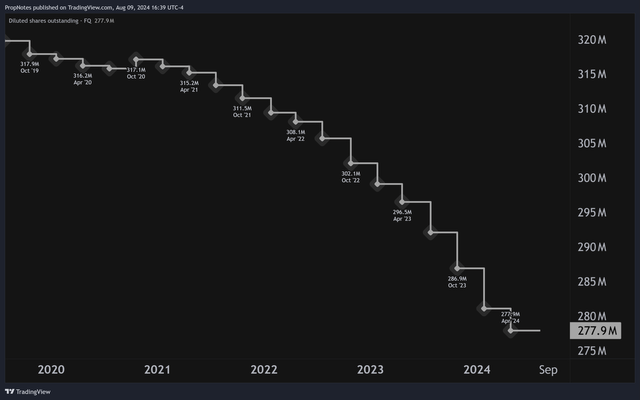

Finally, in terms of earnings per share, management has been incredibly aggressive in buying back shares, as you can see below:

TradingView

From here it is a simple formula:

- Margins remain high

- Sales are rising again

- The number of releases is decreasing

If these things happen, which we think is very likely, then we could easily see Over 20% EPS growth by 2030 on the back.

Deere’s Rating

The growth aspect is interesting, but how expensive are stocks currently?

Interestingly, the stock prices are not designed for this case at all. Currently, DE is trading at a GAAP P/E of 10, which we believe clearly puts it in the “value” category:

I’m looking for Alpha

At this price, the company is expected to experience incredibly low growth in the coming years, which, as explained above, we do not consider likely.

From a market sentiment perspective, the company has made great progress on margins since 2022, but the stock has remained stagnant:

TradingView

It may take a while for the markets to sufficiently “digest” a big move, but given the points mentioned above, we do not believe this stagnation can continue much longer.

We know that the agricultural sector is not looking particularly rosy right now and that investors may be worried about the economy. However, by believing this without looking closely, many investors are missing what is right in front of them.

In our view, it is possible that DE can see over 100% upside potential over the longer term if the multiple increases and earnings per share grow double-digit by 2030.

In the short term, we expect an increase in the share price of DE at least to all-time highs sometime over the next 6 quarters. By then, we believe the sentiment issues in agriculture will have been resolved, sales will pick up, and earnings per share will increase significantly as more dollars hit the bottom line.

The only other competitor in DE’s weight class is Caterpillar (CAT), which trades at a much higher valuation and has similar near-term growth issues. For our money, DE seems like a more attractive pick.

Overall, we believe DE shares are fantastically cheap and should offer consistent short-term, medium-term and long-term upside potential over the next few years.

Risks

There are some risks to consider when investing in Germany.

First of all, DE is facing lawsuits related to the “right to repair” movement. In late 2023, courts sided with farmers against DE and have done so again recently. It is unclear what exact impact these lawsuits might have on DE’s margins, but the company is fighting back tooth and nail, so it’s fair to say that if the company is forced to pay compensation, it will have a negative impact on shareholders.

Second, if revenues do not pick up again next year, our EPS growth forecasts are unlikely to materialize. This is a risk to growth, but the impact on the stock is likely to be somewhat muted as the current price is already cheap.

Finally, results will be announced in a few days. Expect volatility and we will have a better idea of where the market currently stands, a few months after the last public update, which we used as a basis.

If the market doesn’t like what it hears, the stock could take a hit in the short term. For us, this could prove to be an interesting entry point, depending on the context, but it is still a risk to be aware of.

Summary

Overall, investing in DE involves risks, but the amazing price and potential EPS growth over the next few years – due to higher revenues and improved margins – should make a purchase at this point in time a very attractive price.

Look for results in a few days, but overall we’re happy with DE’s performance and give it a Strong Buy rating. If you want to wait to consider a position until results are released, that makes sense too.

Good luck out there!

This article was written as part of Seeking Alpha’s Investment competition “Best growth idea”which runs until August 9th. With cash prizes, this competition, which is open to all analysts, is one you don’t want to miss. If you are interested in becoming an analyst and entering the competition, Click here to learn more and submit your article today!” –