")

PM Pictures

Investment thesis

In a lower interest rate environment, dividend-paying stocks often perform better as investors look for higher yields than those offered by fixed income investments. With bonds becoming less attractive, these stocks become an attractive alternative, which drives up their performance. Therefore, I believe that lower Interest rates will improve the performance of dividend-paying stocks. This article will explore this dynamic in more detail, focusing on the IGRO ETF and related macroeconomic factors, and why I believe this ETF will outperform.

Fund description and performance

The fund aims to replicate the performance of the 399-constituent Morningstar Global ex-US Dividend Growth Index. The ETF invests in securities with a history of uninterrupted dividend growth and sustained growth (at least five years of consecutive dividend growth). The consensus earnings forecast must be positive and the forward-looking dividend payout ratio must be less than 75%. The method thus ensures future dividend growth.

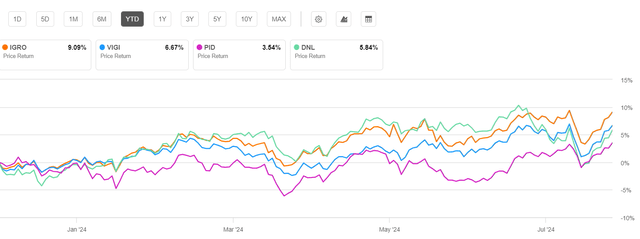

Below is a summary table showing expense ratio and dividend frequency. In addition, I have also included the year-to-date price performance of 9.5%. This return is good but still lower than the S&P 500 index price and total return of 13% and 14.89% respectively. I believe this is due to the lower allocation to the technology sector and the country share outside the US.

Price-performance (Search Alpha)

Investments and sector weightings

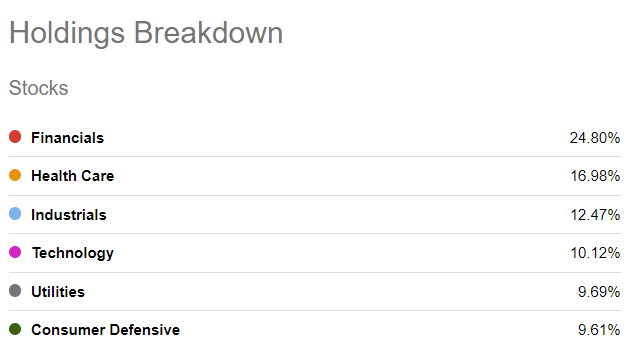

The three largest holdings of the four funds shown below are healthcare stocks, and the second largest sector weighting is in healthcare at 16.98%, with $134 million of the $788 million in assets under management invested in the sector.

The 4 largest fund investments (Search Alpha) Sector breakdown (Search Alpha)

The healthcare sector is considered a safe and stable investment during bear markets. It is considered a defensive late-cycle investment because it can protect a portfolio when the stock market becomes volatile. Here’s why:

Essential services: Regardless of the economic situation, people continue to depend on medical care, medicines and other health services.

Stable earnings: These companies often have reliable earnings and cash flows, which is attractive to investors seeking security in difficult market times.

Dividend payments: Regular dividend payments make them attractive to investors who want a stable income, especially when investments such as bond yields decline in value.

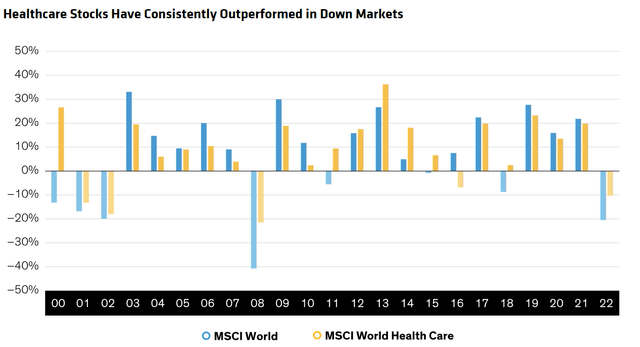

If we compare a healthcare index to a standard world index, it is easy to see the usefulness of defensive healthcare investing. For example, in 2008 and 2022, the MSCI World Healthcare Index fell by half the decline of the MSCI World Index. This shows how healthcare maintains its trend of reducing downside risk. In fact, since 2000, healthcare has outperformed the market every time global equity prices have fallen.

Healthcare vs. World Index (AllianceBernstein)

Macro background

Dividend stocks tend to perform well during periods of macroeconomic volatility and government interest rate cuts as investors look for alternatives to bonds to gain a yield boost. While dividend payments may grow more slowly than a stock’s appreciation, investors can be confident that rising dividend yields will compound returns over time. The effect of compounding, especially when reinvesting dividends, can make this an extremely lucrative strategy.

When the Federal Reserve begins cutting interest rates, companies that continue to increase their dividends have historically typically outperformed other stocks. In contrast, during periods of high interest rates, investors often favor other short-term income-producing assets with minimal risk. For example, after the inflation spike largely triggered by the invasion of Ukraine, which led to significant price increases in everyday consumer goods, Chairman Powell was forced to implement a series of consecutive interest rate hikes to counteract the effects of inflation (basic economic theory that I will not get into in this article). This caused the yield on the 10-year Treasury note to rise from 1.72% to 5%. During this time, money market funds saw a 21% increase in assets under management as investors gravitated toward high-yielding cash equivalents with little to no risk, often at the expense of dividend stocks, whose valuations came under pressure.

Because dividends contribute significantly to total returns, investors might consider focusing on stocks that increase their dividends when the Fed cuts rates, especially when income is a priority. In addition, dividend-paying companies have historically served as a hedge against market uncertainty because management is generally cautious about changes in payout ratios. This stability becomes even more attractive during times of heightened economic and political uncertainty.

Such companies are often referred to as “dividend aristocrats” because the methodology for such indexes only includes companies that have increased their dividends for 25 years or more in a row. A recent study by Ed Clissold and Thanh Nguyen of Ned Davis Research provides empirical evidence of this. They found that, on average, dividend-paying stocks tend to outperform non-dividend-paying stocks, starting several months before the first rate cut in a Fed easing cycle and six to nine months after the cut.

I consider this to be a key reason for my buy recommendation for this ETF. Macroeconomic factors significantly impact dividend growth strategies because lower interest rates allow companies to borrow more cheaply, which reduces the likelihood of dividend cuts. In addition, an inverted yield curve increases the likelihood of a recession, which in turn increases the likelihood of further rate cuts.

Why international dividends

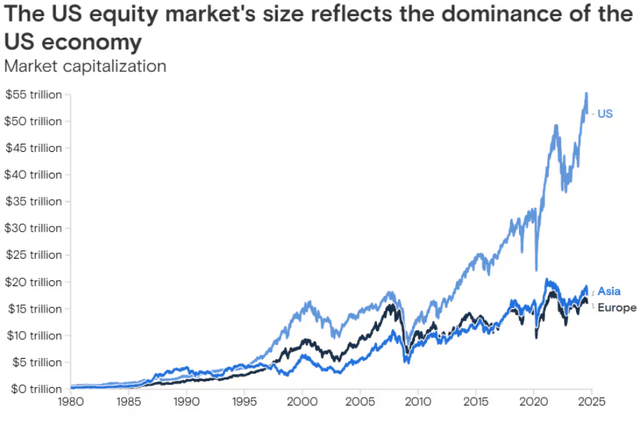

As the following graph shows, the US stock market has grown significantly compared to other stock markets since the 2008 financial crisis.

Size of the US stock market (Goldman Sachs)

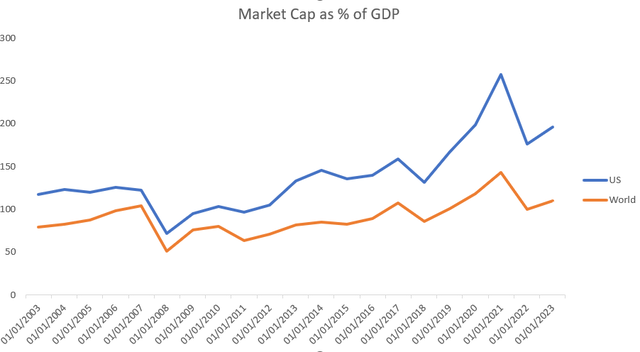

Although the U.S. has long had the largest stock market and economy, the gap between it and other markets has widened since the financial crisis. This discrepancy is due to the fact that the U.S. has experienced a more robust recovery compared to the rest of the world. In addition, the total market capitalization in the U.S. has grown relative to GDP, indicating that the value of the stock market has increased relative to the country’s economic growth. In contrast, this ratio has remained relatively stable in the rest of the world. The U.S. market capitalization has increased by 70% since 2003, while the world market capitalization has only increased by 39%.

Market capitalization % of GDP (Bloomberg)

This trend is not surprising as US companies, particularly in the technology sector, have experienced much higher earnings growth compared to their global peers. However, this has also led to inflated market valuations relative to non-US companies, so I believe this underscores the importance of geographic diversification as an investment strategy.

I have always been a strong advocate of dividend payments from companies outside the US, as some of the longest-running dividend-paying companies are based outside the US. This, coupled with the fact that European markets have lagged behind the US, reinforces my belief that returns should also be sought outside the US market.

Comparisons with other providers

I have compared several ETFs similar to IGRO and IGRO consistently outperforms the others while maintaining the lowest fees. IGRO’s year-to-date performance is 9%, which is significantly higher than its peers, whose returns range from 3% to 6%. Over the past year, IGRO has also been the group’s top performer with a performance of 15.74%, followed by VIGI at 14%.

Comparison with competitors (Search Alpha)

Additionally, IGRO’s turnover (a measure of the ETF’s trading volume) is at the low end of its peers at 38%. Less trading means lower transaction costs, which have a positive impact on performance over a long period of time. Additionally, IGRO’s 3- and 5-year betas are 0.92 and 0.98, respectively, closely matching the category average of 1, suggesting minimal market volatility. This is crucial for investors seeking a stable dividend yield with minimal risk.

Risks

As with any investment, there is always a risk of being wrong. A significant problem here is that the portfolio is somewhat concentrated. With only 399 constituents, it is relatively small and therefore exposed to individual stock risk. This means that disappointing earnings from just a few companies could negatively impact the price of the ETF. Additionally, because this ETF excludes US stocks, particularly US technology stocks, it could miss out on short-term sector gains. While I have noted that this sector and the broader US market could be overvalued, there is always a chance that markets could continue to rise in the short to medium term.

Diploma

Overall, this article explains why investing in a diversified international dividend growth ETF is a smart strategy, especially considering the macroeconomic environment, interest rate cuts, and comparisons with peers.