")

A boy and the sea/E+ via Getty Images

Provision of protein solutions

The thesis surrounding Simply Good Foods (NASDAQ: SMPL) Investments are based on the growing desire for leaner sources of protein and fiber without the additional energy calories from carbohydrates or Fat. In a world of rising healthcare costs, obesity and limited access to nutritious and satisfying food, the idea of losing weight is a growing problem. Some people turn to GLP-1, others to more exercise to offset the flood of calories, but the real cause may be diet.

Many studies show that increased consumption of lean protein sources such as chicken, fish, egg whites and whey protein has led to a reduction in waist circumference, which is a leading indicator of many health problems. Although these types of foods are already available, we still struggle with obesity problems today. Food is is inherently addictive, especially when it is scientifically designed to be so, and eating chicken and broccoli at every meal your entire life can be unsatisfying.

Simply Good Foods Company is taking on this challenge with a unique approach. SMPL is a consumer packaged goods company committed to the healthy snacking movement. It offers a range of trusted brands that provide convenient, innovative and delicious snacks and meal replacements, as well as other product options to promote health. The brands typically offer products that are high in protein and fiber and low in carbohydrates and fat.

Brand names in the portfolio include Atkins Nutritionals (based on the Atkins diet), Quest Nutrition and the newly acquired Only What You Need (OWYN), a plant-based protein shake brand. The acquisition of OWYN was announced in late April and closed on June 13, so it has no impact on this quarter’s financials.

With the Quest brand, they aim to offer a diverse range of protein bars, cookies, protein chips, savory snacks, ready-to-drink (“RTD”) shakes and confectionery that meets current and emerging consumer trends. Likewise, the Atkins brand focuses on providing a wide range of protein bars, RTD shakes, cookies, protein chips, savory snacks and confectionery.

Thanks to their powerful sales, marketing, research and development teams, we are able to distribute these products nationwide through various retail channels, including mass merchandisers, grocery stores, drug stores, club stores, e-commerce platforms and smaller retail outlets such as convenience stores and gas stations.

Overall, I really like SMPL brands. I eat Quest bars and chips daily and I really like the OWYN formula as I’m not usually a fan of plant-based diets. I think the business model of selling accessible high protein/low carb solutions also adds tremendous value to society. However, I find some weaknesses in the valuation and the moat to proceed with a buy recommendation. I hold a small amount but I don’t plan on adding to it until I see any of these risks improve.

Review of the 3rd quarter of the 2024 financial year

On June 27, 2024, Simply Good Foods reported its earnings for the third quarter of the fiscal year ended May 25, 2024. The OWYN acquisition was announced in late April and closed on June 13, so it has no impact on this quarter’s financials. Here’s a breakdown of some highlights from last quarter’s results that will help with future evaluation:

revenue

- Revenue was $34.84 million, up 1% year over year, primarily due to volume growth at Quest Nutrition.

- Sequential sales growth was 7.2%.

Geographical performance

- Sales in North America increased 3.2% year-on-year.

- International sales fell by 2.4% compared to the previous year.

- About 98% of the company’s sales come from North America. The largest international markets are Australia and New Zealand, after Quest Nutrition withdrew from the European protein bar market.

Margins

- Gross margins were 39.9%, up 320 basis points year-on-year and 250 basis points quarter-on-quarter.

- The improvement in margins resulted from lower costs for ingredients and packaging.

Retail sales activity

- In the 13 weeks ending May 26, 2024, retail takeaways in measured U.S. channels increased 2.9%.

- Taking into account measured and unmeasured channels, the estimated growth in takeaway retail is 5%.

- The portfolio’s overall performance is below the 6.4% average growth in the nutritional snacks category, mainly due to the underperformance of Atkins, which impacts Quest Nutrition.

Brand performance

Atkins Diet

- Measured retail sales in the United States fell 9% year-on-year.

- When combining measured and unmeasured channels, the decrease was about 5%.

- Amazon reported 16% year-over-year growth for the Atkins brand.

- Consumer surveys show that 80% of people are interested in losing weight or eating healthy, and the Atkins diet is well positioned as a proven low-carb, low-sugar solution.

- The company is in the midst of a five-point revitalization plan for Atkins and expects full results next year.

- The first signs of a positive impact of the plan are evident: there is a slight improvement compared to the previous quarter.

Quest Nutrition

- Accounts for over 60% of portfolio turnover.

- Retail pickup in observed channels increased by 13.5% year-on-year.

- The snack segment saw retail sales grow by 27%, with salty snacks such as Quest chips growing by around 50%.

- Although Quest bars are still popular on Amazon, e-commerce growth slowed slightly to 16% year-over-year.

- The company plans to drive bar innovation in the second half of 2025 and expand the salty snacks segment with new flavors and packaging types.

- Quest Chips now account for about 25% of Quest Nutrition’s total sales and bring in a significant number of new users.

OWYN (Only what you need)

- The acquisition was completed on June 16, 2024.

- Retail takeaway growth was 117.5% for the quarter.

- It is expected to contribute $25 million to $30 million to net sales in the fourth fiscal quarter.

- Net sales are expected to reach $120 million in calendar year 2024, with the potential to double in the next four years.

- Growth strategies include expanding distribution, improving product formulas and introducing new product formats such as bars and chips.

- OWYN increases its portfolio exposure in the liquid prepared food segment by around 400 basis points to 23% of total sales.

- Mark Olivier, CEO of OWYN, will join Simply Good Foods’ leadership team to ensure a smooth integration and effective growth.

Valuation risk

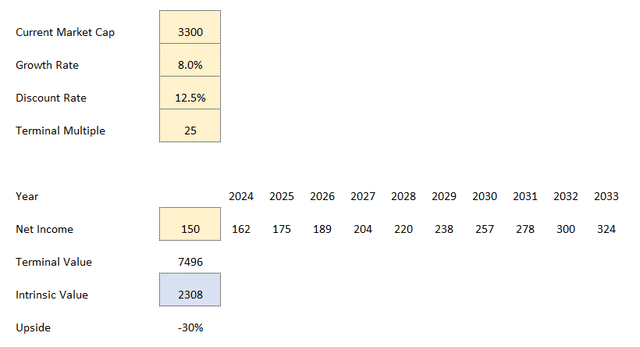

It looks like SMPL is growing its Quest and OWYN brands pretty well, while Adkins is lagging behind, so I’ll use a moderate growth rate that’s in line with analyst estimates for the valuation. For the model, I used a discounted income strategy.

SMPL-Discounted Income Model (Author)

I took TTM net profit and increased it by a healthy 8%. That’s well in line with analysts and my own assumptions about the protein market. As a small margin of safety, a 12.5% discount rate was applied to future earnings. Then I applied a very decent P/E of 25, since SMPL’s historical range is anywhere from 20 to 30 depending on the growth rate. Personally, I think these are pretty optimistic estimates that don’t take competitive risks into account. Even then, I’m left with an intrinsic market cap value of 2.3B at a current value of 3.3B. That represents 30% downside risk from the current share price. I didn’t even apply net debt to that value, although it’s not large anyway due to the capital-light structure.

Competitive risk

As mentioned, SMPL operates a capital-light model where they own the brands, marketing, and product development, but outsource the manufacturing process. That means the company stands or falls on branding and solutions. That works wonderfully when the brands remain strong, but can spell disaster when new entrants enter the market or tastes change. There are many high-protein brands on the market right now, like Think, Optimum Nutrition, Premier Protein, Barbells, Power Crunch, and the list goes on. The CPG market is quite volatile, and I would want to pay a lower price for SMPL if I made it a large part of a portfolio. That said, it still seems like a solid company.

They have a significant position of insider ownership, a focused target on the protein market, which should drive efficiency and sustain higher margins, low debt and continued growth. I believe SMPL will go down the path of being a serial buyer of these protein brands to further diversify. Since I am quite bullish on this specific market, I hold a small position.