MILWAUKEE – Sometimes we put pressure on ourselves to earn or save more money after a certain age. How much should we have saved by the time we’re 20, 30, or 50? We asked an expert to help us navigate life’s financial milestones.

Kiana Ayala is still looking for her dream home.

“We wanted to find a house close to my boyfriend’s work,” she said as she strolled through Milwaukee’s Johnson’s Woods neighborhood.

In August, Ayala made an offer that was $2,000 over asking price on a 3-bedroom, 1-bath ranch home. But after looking further, she decided it wasn’t the right fit. Ayala has been saving for more than a year and a half to become a first-time homeowner.

“If I’m honest, saving is like a muscle I had to develop,” Ayala said.

Ayala reduced the things she didn’t need. Instead of going out to restaurants for dinner, she cooked for herself. An evening with friends became an evening at home.

“I set a goal to own a home by the time I was 30,” Ayala said. “My 20s were like the transition into adulthood. I just wanted time to figure out how to live my life, for lack of a better word.”

SIGN UP TODAY: Get daily headlines and breaking news alerts via email from FOX6 News

The burden of her own expectations began to take its toll.

“If you don’t take those steps as quickly as some other people, you can start to doubt yourself,” Ayala said.

According to experts, this is where most of us make a mistake when trying to achieve life’s financial milestones. Don’t compare your finances to others’. Instead, give your money meaning.

“The more time you spend thinking about why money is important to you and using those resources on the things that matter most to you, I believe the greater your chances of living a more fulfilling and happier life,” says Joe Maier, senior vice president and director of wealth management at Johnson Financial Group.

Most of his clients are in their 50s or 60s. Here’s what Maier wishes he could tell them if they had walked through his door decades earlier:

“We should be having conversations with every college graduate in their 20s saying to try to base their budget on 80% of their income – or 90% of their income,” Maier said. “If you can develop that discipline and put money aside and provide for your future self, you’ll be really happy when you’re 45 or 55 with the opportunities you have that you wouldn’t have had otherwise.”

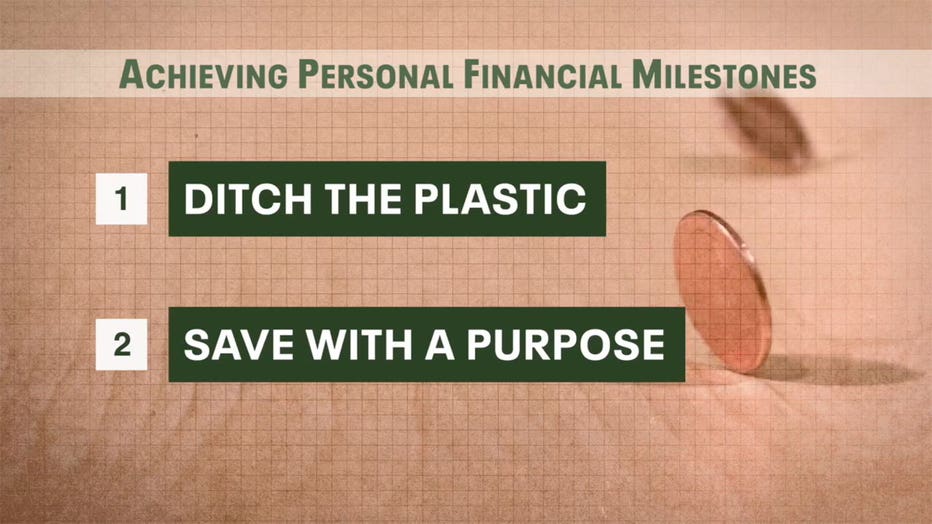

Maier gave us his “two cents” on how to do that, even if you’re living paycheck to paycheck. First, he says, throw away the credit card. Pay off your credit card debt and stop using it unless you have money set aside to cover it. Second, save with intention. Be clear about what you’re saving for – whether it’s for retirement, a better life for your kids or, like Ayala, a dream home. Maier says that makes it easier to set financial goals.

“It’s less about a number than about habits,” Maier added.

“I want it to be ready to move in,” Ayala told us in front of a house for sale. “We didn’t want to move in and have to fix the roof or the plumbing.”

FREE DOWNLOAD: Get breaking news in the FOX6 News app for iOS or Android

Ayala’s search only intensified. Her real estate agent urged her to take a home buying course. She said she enjoyed saving money. Her dream is now a lot closer to becoming a reality.

“If you want your future self to be somewhere, your present self has to start doing the work,” Ayala said.