")

salajean/iStock via Getty Images

Barrick Gold (NYSE:GOLD) just reported its second-quarter results, and its stock shot up more than 9% the day after the release.

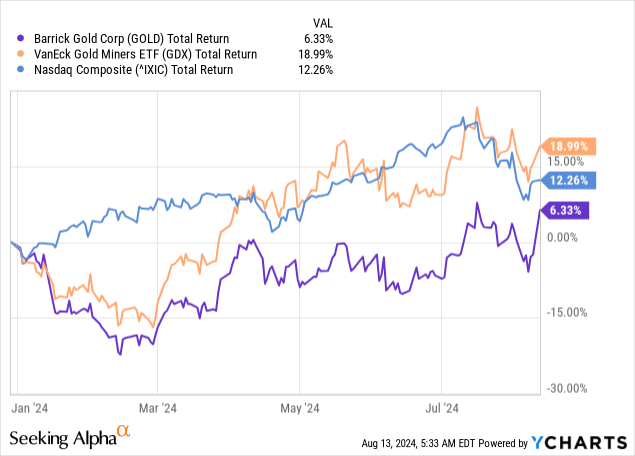

Although the market was surprised by the better than expected results, the quarter was not Reason enough to be optimistic about the stock. Even after the almost double-digit increase in the share price, the performance gap between GOLD and the VanEck Gold Miners ETF (GDX) is still very broad and not in favour of gold miners.

A good quarter does not necessarily make a trend and unfortunately GOLD remains inferior compared to other large-cap gold mining stocks.

Precious metal prices are likely to continue to be an important tailwind for Barrick, but at the moment it is too early to say whether The company is on the right track.

A good quarter, but not enough

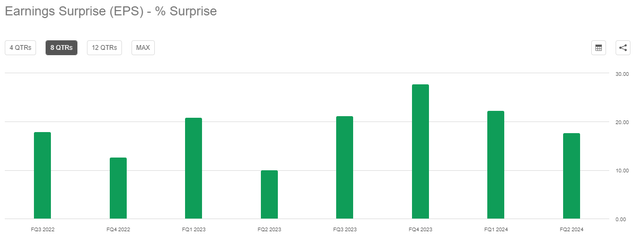

For the second quarter of 2024, Barrick management reported earnings per share (EPS) that exceeded analysts’ consensus estimates. Adjusted net earnings per share for the three-month period were $0.32, while analysts had expected $0.27.

As can be seen in the chart below, the earnings surprise was quite significant, suggesting that sell-side analysts underestimated Barrick’s ability to capitalize on recent price increases in gold and copper.

I’m looking for Alpha

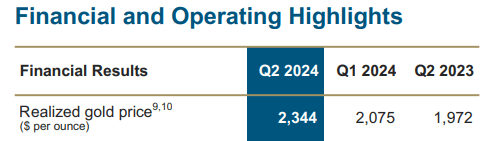

Gold production, on the other hand, recorded a year-on-year decline, more than offset by an increase in the realized gold price from USD 1,972 in the second quarter of 2023 to USD 2,344 in the second quarter of 2024.

Barrick Gold Investor Presentation

Barrick Gold earnings release

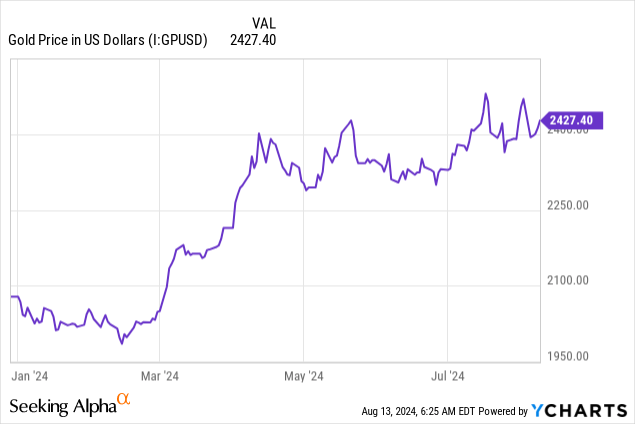

The magnitude of the gold price increase in the second quarter of this year can be seen in the chart below and was a major tailwind not only for Barrick but also for other gold miners.

So far, the price of precious metals has continued to rise in July and August and should remain a key tailwind for Barrick’s EPS numbers next quarter. However, the magnitude of the increase is much smaller compared to the increases seen earlier this year, a sign that gold production and costs will be far more important in the second half of 2024.

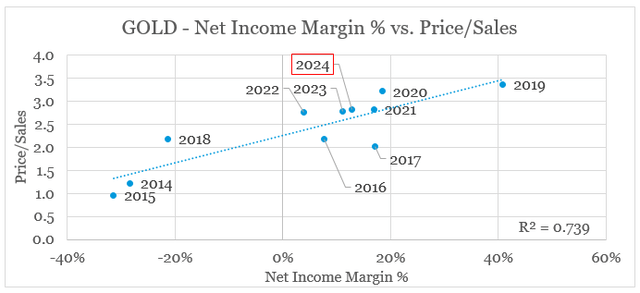

In addition, Barrick stock now trades at a revenue multiple equal to the company’s net profit margin for the trailing 12-month period. This now becomes a limiting factor for GOLD’s returns for the remainder of 2024 unless we see a significant improvement in margins.

prepared by the author, using data from SEC filings and Seeking Alpha

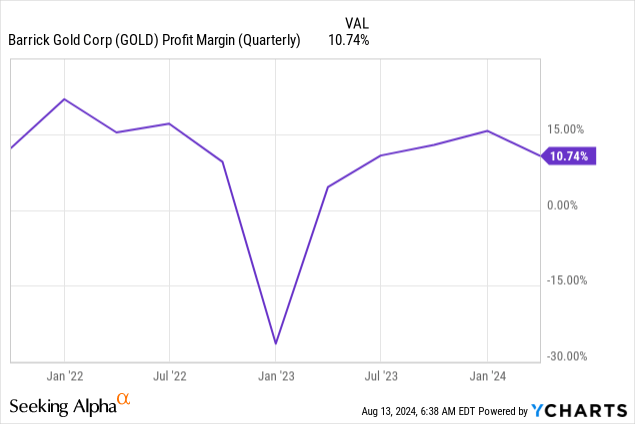

As costs continued to rise last quarter, Barrick’s quarterly net profit margin appears to have peaked back in the fourth quarter of last year. This development now puts the current revenue multiple at risk if total costs continue to rise faster than the gold price for the remainder of 2024.

Worse choice

The other big problem investors face with Barrick Gold is that even if they assume the price of gold continues to rise at the same rate it did in the first half of 2024, they would probably be better off with other large-cap gold miners.

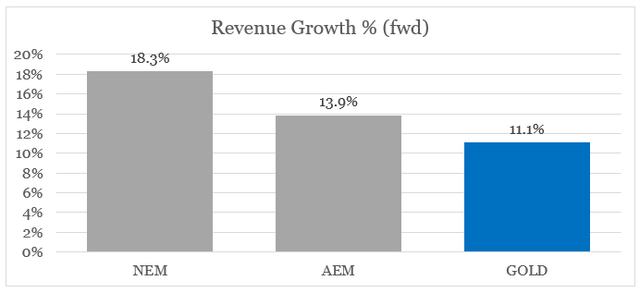

As a starting point, GOLD has the lowest expected revenue growth compared to its main competitors Newmont (NEM) and Agnico Eagle Mines (AEM).

created by the author using data from Seeking Alpha

The reason expected growth is so important in this case is because it is critical for mining companies to have the ability to expand their production during times of high margins.

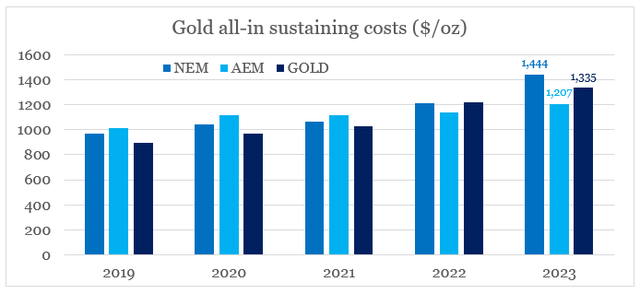

This brings us to the second reason, which is cost. In 2019, Barrick Gold was among the lowest cost producers, but that has changed in recent years as Agnico completed a series of groundbreaking M&A deals. Newmont is now the highest cost producer of the three, but that could soon change.

prepared by the author, using data from annual reports

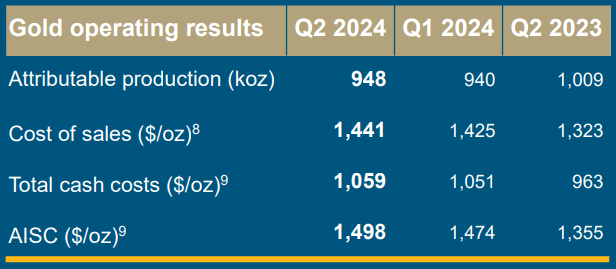

In recent quarters, Barrick’s total operating expenses (AISC) increased significantly to $1,498 in the last reported quarter, representing an increase of 11% year-on-year.

Barrick Gold Investor Presentation

This is significantly higher than the current guidance for fiscal 2024, where AISC is expected to be in the range of $1,320 to $1,420. Therefore, unless costs come down significantly in the second half of the year, we will likely see a revision to Barrick’s guidance for the remainder of 2024.

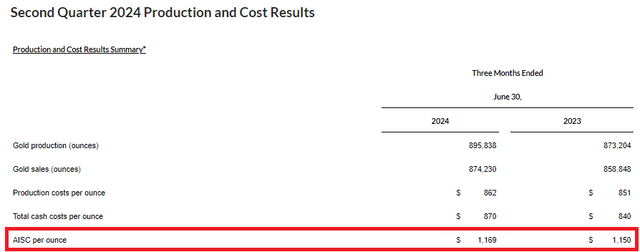

In comparison, Agnico Eagle Mines reported only a marginal increase in AISC in the second quarter of 2024, with costs increasing by just 2% compared to the same quarter last year.

Agnico Eagle Mines: Q2 2024 Earnings Release

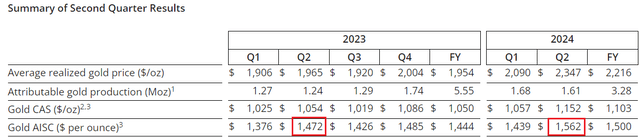

Newmont remains the highest-cost producer, even though its AISC increased only 6% in the second quarter of 2024, almost half the percentage increase at Barrick.

Newmont: Q2 2024 earnings release

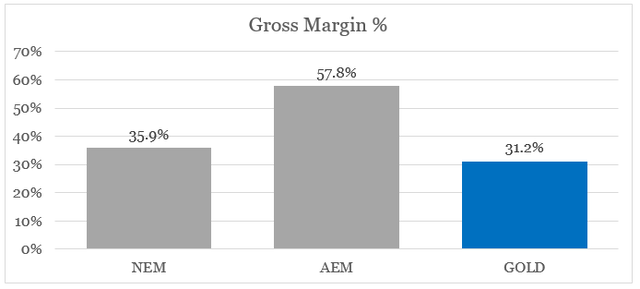

However, when comparing REVALUATION to GOLD, the latter still has a lower gross margin, which has a significant impact on profit growth in good times when the gold price soars.

created by the author using data from Seeking Alpha

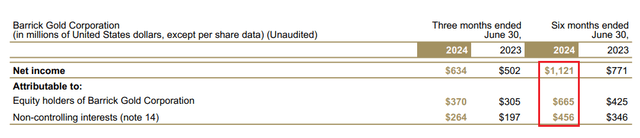

Another major disadvantage of Barrick is the significant amount of non-controlling interests. For example, in the last 6-month period, a total of $456 million was attributed to non-controlling interests, which represents about 40% of the company’s total net income. At Newmont, the same amount for the first half of 2024 is negligible.

Barrick Gold: Q2 2024 earnings release

Diploma

Based on all of the above, GOLD will likely continue to underperform peers as costs continue to rise. Even if gold prices stay at their current trajectory through the end of 2024, investors would likely be better off sticking with higher-quality mining companies like Agnico Eagle Mines. On the other hand, if gold prices remain stagnant or even fall through the end of 2024, Barrick’s margins would suffer, limiting any potential upside for the rest of the year.